Stocks cruise at a high altitude – What's next

Investors that have taken a principled approach to investing and have adhered to a long-term investment plan reaped gains in 2020 and have continued to be rewarded in 2021. More importantly, they are making progress toward their financial goals.

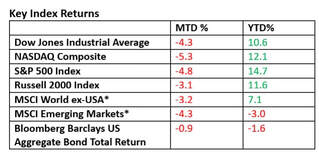

As the first half of the year ended, the S&P 500 Index, which is a broad-based index of 500 larger U.S. companies, ended June at a record high. The better known Dow Jones Industrials, which is made up of 30 large firms, finished the first half with a strong gain of nearly 13%. Meanwhile, the Russell 2000 Index of smaller companies is up an impressive 17% for the first six months of the year.

As the first half of the year ended, the S&P 500 Index, which is a broad-based index of 500 larger U.S. companies, ended June at a record high. The better known Dow Jones Industrials, which is made up of 30 large firms, finished the first half with a strong gain of nearly 13%. Meanwhile, the Russell 2000 Index of smaller companies is up an impressive 17% for the first six months of the year.

Source: MSCI.com, Bloomberg, MarketWatch

MTD: returns: May 28, 2021-June 30, 2021

YTD returns: Dec 31, 2020-June 30, 2021

*in US dollars

Where might we be headed for the rest of the year? While we can use history as a guide, let’s also acknowledge that past performance is no guarantee of how we might perform going forward. I think that is something we all understand, but it bears repeating.

That said, please follow me as I briefly dive into the numbers. Using data from our friends at LPL Research, we learn that bull markets that have emerged from a bear market of at least a 30% decline have had strong returns in the first year. The rally that followed 2020’s bear market (a 34% decline) is no exception.

The average increase in the six bull markets since WWII that followed a 30% or greater decline was 41% in the first year. It’s an impressive one-year return and is a reminder that bear markets usually end unexpectedly. Those who are safely in cash during the decline can find themselves chasing returns.

The first year increase of 75% from 2020’s bottom ranks as number 1, exceeding 2009’s second place return of 69%. On average, all the bull markets in question have been positive in year two, with an average return for the S&P 500 of 17%.

However, year number two has not been without volatility, with an average pullback during the second year of 10%. Thus far, we have yet to see a meaningful pullback in the broader market indexes, but we are only three months into year two.

What helps drive returns? Momentum, an expanding economy, higher corporate profits, and a generally accommodative policy from the Federal Reserve. Those variables are in place today. But every cycle has its own peculiarities. This year is no different.

The economy has never experienced the kind of lockdown and reopening we are seeing today. It’s uncharted economic territory. So far, growth has been much stronger than most forecasters expected. We can credit massive fiscal stimulus, the reopening of various sectors of the economy, pent-up demand, and the easing and end of social distancing restrictions.

But the benefits have been spread out unevenly. Inflation also remains a concern, though the recent drop in Treasury bond yields suggests that most investors seem to view the recent surge in prices as temporary. We could also see the rate of growth peak in the second quarter as fiscal stimulus begins to wane.

It’s why we default back to the financial plan. It’s the cornerstone of our approach. The short-term traders will react to unexpected events, both positive and negative. But let’s be careful about following their lead. What can impact stocks today can be forgotten by investors tomorrow.

I trust you’ve found this review to be educational and informative. Let me emphasize that it is my job to assist you. If you have any questions or would like to discuss any matters, please feel free to give me a call.

MTD: returns: May 28, 2021-June 30, 2021

YTD returns: Dec 31, 2020-June 30, 2021

*in US dollars

Where might we be headed for the rest of the year? While we can use history as a guide, let’s also acknowledge that past performance is no guarantee of how we might perform going forward. I think that is something we all understand, but it bears repeating.

That said, please follow me as I briefly dive into the numbers. Using data from our friends at LPL Research, we learn that bull markets that have emerged from a bear market of at least a 30% decline have had strong returns in the first year. The rally that followed 2020’s bear market (a 34% decline) is no exception.

The average increase in the six bull markets since WWII that followed a 30% or greater decline was 41% in the first year. It’s an impressive one-year return and is a reminder that bear markets usually end unexpectedly. Those who are safely in cash during the decline can find themselves chasing returns.

The first year increase of 75% from 2020’s bottom ranks as number 1, exceeding 2009’s second place return of 69%. On average, all the bull markets in question have been positive in year two, with an average return for the S&P 500 of 17%.

However, year number two has not been without volatility, with an average pullback during the second year of 10%. Thus far, we have yet to see a meaningful pullback in the broader market indexes, but we are only three months into year two.

What helps drive returns? Momentum, an expanding economy, higher corporate profits, and a generally accommodative policy from the Federal Reserve. Those variables are in place today. But every cycle has its own peculiarities. This year is no different.

The economy has never experienced the kind of lockdown and reopening we are seeing today. It’s uncharted economic territory. So far, growth has been much stronger than most forecasters expected. We can credit massive fiscal stimulus, the reopening of various sectors of the economy, pent-up demand, and the easing and end of social distancing restrictions.

But the benefits have been spread out unevenly. Inflation also remains a concern, though the recent drop in Treasury bond yields suggests that most investors seem to view the recent surge in prices as temporary. We could also see the rate of growth peak in the second quarter as fiscal stimulus begins to wane.

It’s why we default back to the financial plan. It’s the cornerstone of our approach. The short-term traders will react to unexpected events, both positive and negative. But let’s be careful about following their lead. What can impact stocks today can be forgotten by investors tomorrow.

I trust you’ve found this review to be educational and informative. Let me emphasize that it is my job to assist you. If you have any questions or would like to discuss any matters, please feel free to give me a call.