September Client-letter: Looking past scary headlines

It's easy to say when stocks are holding up or moving higher. But a jarring correction may create uneasiness, as some of you have shared with me. I can't help but be reminded of a comment by John Bogle, retired CEO and founder of the mutual fund giant, The Vanguard Group. "Don't pay a lot of attention to the volatility in the market place. All these noises and jumping up and down along the way are really just emotions that confuse you." [read article]

The question shouldn't be, "Will my investments go up or down?" They will. Instead, ask, "Will the fact that investments go up and own bother me enough to do something dumb?" In other words, Bogle is saying that volatility is part of the DNA of the market. Stocks go up, and stocks go down. Historically, stocks have gone up a lot more than they have gone down. But from time to time, they do go down.

Stock market corrections, defined as a decline of 10% to 20% of a major market index–typically the S&P 500 Index–are a normal part of the investment landscape. In the context of an expanding economy, they are healthy when valuations get a bit extended, as they wipe out excess enthusiasm, reduce valuations, and set the foundation for another round of gains.

Yes, I know it sounds a bit clinical, and recent volatility has been unsettling. I recognize that. But swings in the market are normal. But let's be clear: Volatility can be managed by investing in a diversified portfolio that seeks out long-term capital appreciation, a modest degree of stability, and income.

Since the May 21 peak in the S&P 500 Index, shares are down 12.35% at their low point in August (St. Louis Federal Reserve). That fits neatly into the definition of a stock market correction. But it's been four years since shares have lost more than 10% (St. Louis Fed), which is an unusually long period.

Such instances may lull an investor into complacency, which adds to the angst when shares fall. Historically, however, 10% declines are more common. In fact, since WWII, a correction has occurred about every 20 months (Dow Jones, Morningstar, Bloomberg, Reformed Broker) so we were overdue. Moreover, the average correction (a 10-20% decline) lasts 71 days, recording a 13.3% decline.

But, you may say, the most recent decline has been sudden and quite potent. Yes, that's true, with the S&P 500 falling more than 10% in just four days! However, since 1940, there were 10 other times when stocks fell at least 10% over a four-day period. Though the S&P 500 sometimes struggled to regain its footing in the immediate aftermath of the decline, the measure of 500 large U.S. firms was up 5.2% on average after 50 trading days and averaged a 20.1% rise within 250 trading days (Charles Schwab).

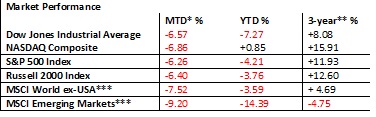

Market Performance

Source: Wall Street Journal, MSCI.com

*July 31, 2015 – August 31, 2015

**Annualized

***USD

What's going on? China and the Fed

It's a question that has come up often in recent meetings and discussions with clients. In reality, it's hard to pinpoint the exact cause for the recent selloff, but first I'll cover some of the negative headwinds.

China is the world's second largest economy, and its growth rate has been slowing. Although China officially announced that Q2 GDP expanded by 7.0% in Q2 (Bloomberg), few believe the official report. The most immediate impact has been in emerging market currencies, which are grappling with China and a possible Fed rate hike. Note from the table of returns that emerging market stocks are among the biggest losers.

In addition, China surprised markets by devaluating their currency on August 11 by about 3% (Wall Street Journal). China's central bank (website press release) billed the surprise announcement as a market-oriented reform and a one-time move. Liberalization is welcome, but the timing seemed to coincide with its sagging economy. In other words, it’s a way for China to boost exports.

Here's the rub–with the exception of the devaluation, China's economy has been slowing for quite some time. So, it's old news that should have been priced into shares. Even the surprise devaluation was quite modest. Declines in other currencies against the dollar over the last year or two have been much more extensive. But there was little reaction in the market.

A second problem–U.S. exports to China make up less than 1% of U.S. GDP (U.S. Census). It's insignificant, so it’s a bit puzzling why stocks would lurch to the downside when the U.S. economy isn't dependent on sales to China. U.S exports to Canada are almost triple those to China (U.S. Census) and our friends to the north have entered a recession (Reuters), but no one's blaming market problems on Canada!

The Federal Reserve is also being blamed for the selloff. In late July and early August, markets seemed resigned to the idea the Fed was set to boost rates at its September 17 meeting, but global instability and conflicting views from various Fed officials have only added to the uncertainty. Will the Fed or won't the Fed hike in September has investors on edge. Nonetheless, like China, this is an old story. The Fed has been aiming at a possible September rate hike for months. The added uncertainty can create anxieties, but in my view, it's hard to pin all of the correction on the Fed.

If not China, if not the Fed, then…

It's not that China and uncertainty at the Fed aren't headwinds. They are. But as mentioned, they were already in the air.

What I believe we may be seeing:

Looking ahead and short-term risks

A continued stream of negative news from China may add to the recent volatility. While the odds that China will allow its currency to float freely are low, such an event would create plenty of angst in emerging market currencies, and that would likely add to the volatility in U.S. stocks.

Meanwhile, the upcoming September 17 Fed meeting looms large. Even if the Fed hikes, it has consistently telegraphed any series of rates hikes will likely be gradual.

The 1994 and the 2004 rate hike cycles did not spell the end of the bull market. I don't believe this one will either.

I believe it is the emotions that are associated with heightened uncertainty that have exacerbated the market's decline.

Bottom line

If you are a number of years from retirement, a drop in the market may provide an opportunity to selectively deploy any excess cash. If you are nearing retirement, your portfolio is adjusted for risk, so it is designed to be less volatile in both up and down markets.

As I've said before, the financial plan we've recommended incorporates market declines. We've recommended a financial roadmap that's tailored to your financial goals. We don't know when we'll run into traffic jams or hit a pothole, but we believe that detours or deviations from the plan will hinder not help your progress.

Patience is the key. As Warren Buffett once said, "No matter how great the talent or efforts, some things just take time. You can't produce a baby in one month by getting nine women pregnant."

But now may also be the time for a self-evaluation. If this selloff has created anxious evenings, we need to revisit. For some, it's easy to express a high degree of tolerance to risk when markets are rising.

Let me reiterate. I understand the swift correction may be disconcerting for some and irresponsible headlines in the media only add to concerns. But markets will correct from time to time. They always have and they always will. Eventually, we will get a bear market, or a 20% decline. It will happen and few will call it in advance. However, the fundamentals at home have been the traditional drivers of U.S. stocks over the medium and longer term. Currently they are favorable, and I believe they will reassert themselves when the dust settles.

So I will counsel again: look past scary headlines.

In closing

I trust that you have found this month’s summary to be beneficial and educational. I always emphasize that as your financial advisor, it is my job to partner with you. If you ever have any questions about what I’ve conveyed in this month’s message or want to discuss anything else, please feel free to reach out to me.

As always, I am humbled that you have placed your trust in my firm. It is something I never take for granted.

John Davidson, CFP®

KylesHill Financial Planning

The question shouldn't be, "Will my investments go up or down?" They will. Instead, ask, "Will the fact that investments go up and own bother me enough to do something dumb?" In other words, Bogle is saying that volatility is part of the DNA of the market. Stocks go up, and stocks go down. Historically, stocks have gone up a lot more than they have gone down. But from time to time, they do go down.

Stock market corrections, defined as a decline of 10% to 20% of a major market index–typically the S&P 500 Index–are a normal part of the investment landscape. In the context of an expanding economy, they are healthy when valuations get a bit extended, as they wipe out excess enthusiasm, reduce valuations, and set the foundation for another round of gains.

Yes, I know it sounds a bit clinical, and recent volatility has been unsettling. I recognize that. But swings in the market are normal. But let's be clear: Volatility can be managed by investing in a diversified portfolio that seeks out long-term capital appreciation, a modest degree of stability, and income.

Since the May 21 peak in the S&P 500 Index, shares are down 12.35% at their low point in August (St. Louis Federal Reserve). That fits neatly into the definition of a stock market correction. But it's been four years since shares have lost more than 10% (St. Louis Fed), which is an unusually long period.

Such instances may lull an investor into complacency, which adds to the angst when shares fall. Historically, however, 10% declines are more common. In fact, since WWII, a correction has occurred about every 20 months (Dow Jones, Morningstar, Bloomberg, Reformed Broker) so we were overdue. Moreover, the average correction (a 10-20% decline) lasts 71 days, recording a 13.3% decline.

But, you may say, the most recent decline has been sudden and quite potent. Yes, that's true, with the S&P 500 falling more than 10% in just four days! However, since 1940, there were 10 other times when stocks fell at least 10% over a four-day period. Though the S&P 500 sometimes struggled to regain its footing in the immediate aftermath of the decline, the measure of 500 large U.S. firms was up 5.2% on average after 50 trading days and averaged a 20.1% rise within 250 trading days (Charles Schwab).

Market Performance

Source: Wall Street Journal, MSCI.com

*July 31, 2015 – August 31, 2015

**Annualized

***USD

What's going on? China and the Fed

It's a question that has come up often in recent meetings and discussions with clients. In reality, it's hard to pinpoint the exact cause for the recent selloff, but first I'll cover some of the negative headwinds.

China is the world's second largest economy, and its growth rate has been slowing. Although China officially announced that Q2 GDP expanded by 7.0% in Q2 (Bloomberg), few believe the official report. The most immediate impact has been in emerging market currencies, which are grappling with China and a possible Fed rate hike. Note from the table of returns that emerging market stocks are among the biggest losers.

In addition, China surprised markets by devaluating their currency on August 11 by about 3% (Wall Street Journal). China's central bank (website press release) billed the surprise announcement as a market-oriented reform and a one-time move. Liberalization is welcome, but the timing seemed to coincide with its sagging economy. In other words, it’s a way for China to boost exports.

Here's the rub–with the exception of the devaluation, China's economy has been slowing for quite some time. So, it's old news that should have been priced into shares. Even the surprise devaluation was quite modest. Declines in other currencies against the dollar over the last year or two have been much more extensive. But there was little reaction in the market.

A second problem–U.S. exports to China make up less than 1% of U.S. GDP (U.S. Census). It's insignificant, so it’s a bit puzzling why stocks would lurch to the downside when the U.S. economy isn't dependent on sales to China. U.S exports to Canada are almost triple those to China (U.S. Census) and our friends to the north have entered a recession (Reuters), but no one's blaming market problems on Canada!

The Federal Reserve is also being blamed for the selloff. In late July and early August, markets seemed resigned to the idea the Fed was set to boost rates at its September 17 meeting, but global instability and conflicting views from various Fed officials have only added to the uncertainty. Will the Fed or won't the Fed hike in September has investors on edge. Nonetheless, like China, this is an old story. The Fed has been aiming at a possible September rate hike for months. The added uncertainty can create anxieties, but in my view, it's hard to pin all of the correction on the Fed.

If not China, if not the Fed, then…

It's not that China and uncertainty at the Fed aren't headwinds. They are. But as mentioned, they were already in the air.

What I believe we may be seeing:

- A middle-aged bull market that is in its seventh year and one that hadn't seen a correction in four years.

- Market internals have been deteriorating, including a narrowing in leadership. This compares to 2013, when we were witnessing a broad-based advance.

- Pricier valuations, which can add to anxieties, and,

- Earnings growth that has slowed thanks to weakness in energy companies and the stronger dollar.

Looking ahead and short-term risks

A continued stream of negative news from China may add to the recent volatility. While the odds that China will allow its currency to float freely are low, such an event would create plenty of angst in emerging market currencies, and that would likely add to the volatility in U.S. stocks.

Meanwhile, the upcoming September 17 Fed meeting looms large. Even if the Fed hikes, it has consistently telegraphed any series of rates hikes will likely be gradual.

The 1994 and the 2004 rate hike cycles did not spell the end of the bull market. I don't believe this one will either.

I believe it is the emotions that are associated with heightened uncertainty that have exacerbated the market's decline.

Bottom line

If you are a number of years from retirement, a drop in the market may provide an opportunity to selectively deploy any excess cash. If you are nearing retirement, your portfolio is adjusted for risk, so it is designed to be less volatile in both up and down markets.

As I've said before, the financial plan we've recommended incorporates market declines. We've recommended a financial roadmap that's tailored to your financial goals. We don't know when we'll run into traffic jams or hit a pothole, but we believe that detours or deviations from the plan will hinder not help your progress.

Patience is the key. As Warren Buffett once said, "No matter how great the talent or efforts, some things just take time. You can't produce a baby in one month by getting nine women pregnant."

But now may also be the time for a self-evaluation. If this selloff has created anxious evenings, we need to revisit. For some, it's easy to express a high degree of tolerance to risk when markets are rising.

Let me reiterate. I understand the swift correction may be disconcerting for some and irresponsible headlines in the media only add to concerns. But markets will correct from time to time. They always have and they always will. Eventually, we will get a bear market, or a 20% decline. It will happen and few will call it in advance. However, the fundamentals at home have been the traditional drivers of U.S. stocks over the medium and longer term. Currently they are favorable, and I believe they will reassert themselves when the dust settles.

So I will counsel again: look past scary headlines.

In closing

I trust that you have found this month’s summary to be beneficial and educational. I always emphasize that as your financial advisor, it is my job to partner with you. If you ever have any questions about what I’ve conveyed in this month’s message or want to discuss anything else, please feel free to reach out to me.

As always, I am humbled that you have placed your trust in my firm. It is something I never take for granted.

John Davidson, CFP®

KylesHill Financial Planning